Introduction

The purpose of the Iraq Governance Performance and Accountability (IGPA) project is to advance effective, accountable, and transparent governance in Iraq. This USAID effort, implemented by DAI, supports the Government of Iraq (GOI) at all levels to better respond to citizen needs by supporting reform initiatives and Iraqi change agents on inclusive governance and public-sector transparency, accountability, and economy. Reform initiatives includes support to improve service delivery functions, public financial management, and open government initiatives. IGPA also supports the GOI and the citizens of Iraq in forming partnerships and collaborative efforts to solve problems jointly. IGPA has four (4) objectives:

-

Enhance GOI service delivery capacity

-

Improve public financial management

-

Strengthen monitoring and oversight of service delivery and public expenditure

-

Support Iraqi change agents (cross-cutting objective)

IGPA also supports the fulfillment of the US Government’s commitment toward decentralization as a means toward achieving the above objectives, particularly the enhancement of the responsiveness of public services to citizens’ needs and the improvement of transparency and accountability in the use of public resources.

Background

Auditing is an important government function to monitor its spending and to safeguard government assets. The Federal Board of Supreme Audit (FBSA) is responsible for conducting audits to enhance public sector and government accountability. The FBSA provides a critical link on financial and budget oversight between parliament and the government, including government agencies, authorities, companies and controlled entities.

The Administrative Financial Affairs Directorate (AFAD) was created to assume responsibility for provincial public financial management as a result of decentralization focusing particularly on the decentralized directorates. One of the key responsibilities of the AFAD is audit and financial control.

The FBSA and the Ministry of Finance should play a critical role in providing guidelines, rules and regulations for AFADs and decentralized directorates to carrying out their internal audit and control functions.

The local audit consultant will work closely with the international audit consultant to review the current system for internal audit and internal control based on the regulations issued by MOF. The local audit consultant will provide recommendations on updating the FBSA and MOF guidelines as needed and in developing a toolkit (manual, guidelines, templates, worksheets) for the AFAD and decentralized directorates to use to effectively carry out their internal audit and internal control responsibilities.

The local audit consultant will then support the international audit consultant to develop a training and capacity building program in internal audit and control in accordance with FBSA and MOF guidelines and procedures. This will be incorporated into the IGPA comprehensive PFM training and capacity building program prepared for improving PFM processes and procedures and building capacity at the provincial level in key Governorate Office units and the decentralized directorates that provide services.

Additionally, the local audit consultant will advise IGPA/Takamul on how to support the AFAD to reinforce its role in the annual financial reporting process with MOF and FBSA. If needed and decided, the local financial audit consultant can assist in drafting a directive to be issued by the MOF on the role of the AFAD in the annual financial reporting process.

Objective:

The main objectives of the local Audit Consultant scope of work are to:

-

Support the international audit consultant to review the current GOI laws, MOF and Federal Board of Supreme Audit rules and regulations on internal audit and control related to the AFAD and decentralized directorates.

-

Work closely with the international audit consultant to review the current system for internal audit and internal control implemented by the AFAD and decentralized directorates and recommend improvements to address any weaknesses or gaps in the system.

-

Support the international audit consultant to develop a targeted training and capacity building program based on the needs of the AFAD and decentralized directorates to effectively carry out their internal audit and internal control functions and responsibilities

-

Support the IGPA PFM advisors to provide internal audit and internal control training and follow up capacity building for staff of the AFAD and decentralized directorates.

-

Advise and support IGPA/Takamul to reinforce the AFAD role in the annual financial reporting process in coordination with the MOF and FBSA

-

Prepare a final progress report.

II. Specific Tasks of the Consultant

Under this Scope of Work, the Consultant shall contribute to performing, but not be limited to, the specific tasks specified under the following categories:

Task1: Review the current GOI laws, MOF and Federal Board of Supreme Audit rules and regulations on internal audit and control related to the AFAD and decentralized directorates. The consultant will work with the international audit consultant to review the current GOI laws, MOF and FBSA rules and regulations on internal audit and internal control. The consultant will support the international consultant to prepare a compilation of all of the relevant current GOI laws, MOF and FBSA rules and regulations as a basis for reviewing the current audit and control system and making recommendations to improve the system in line with best practices and adapted for local context.

Task 2. Assess the current capacity of AFAD and decentralized directorates in internal audit and internal control. The consultant will conduct an assessment of the current state of the AFAD and decentralized directorates in audit and control. The assessment will review the organizational structure and the staffing, roles and responsibilities, process and procedures according to current GOI laws and regulations for external auditing function and assess how well the AFAD and decentralized directorates are executing the auditing and control function, identify gaps and weaknesses in the current system and recommendations for improving the audit and control system. The local consultant will support the international consultant to discuss the assessment findings with the AFAD and decentralized directorates officials and staff for feedback and finalize the assessment report as needed.

Task 3: Develop a targeted training and capacity building program based on the needs of the AFAD and decentralized directorates to effectively carry out their internal audit and internal control functions and responsibilities. Based on the assessment findings, the local consultant will support the international consultant to develop a targeted training and capacity building program for the AFAD and decentralized directorates to build staff capacity in auditing and internal control and strengthen the institution.

Task 4. Provide internal audit and internal control training and follow up capacity building for staff of the AFAD and decentralized directorates in collaboration with the PFM advisors. The consultant with the support of the PFM advisors will conduct audit and control training sessions for AFAD and decentralized directorates and follow up capacity building for the staff according to the training and capacity building program developed under Task 3.

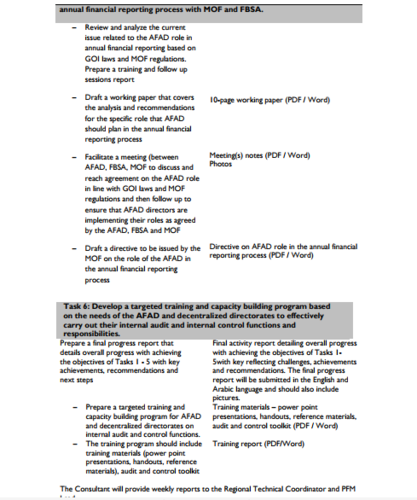

Task 5. Advise and support IGPA/Takamul to reinforce the AFAD role in the annual financial reporting process with MOF and FBSA. The local audit consultant will work with the PFM advisors to assist AFAD directors to review and analyze the current issue related to the AFAD role in annual financial reporting based on GOI laws and MOF regulations. The local financial audit consultant will then support the PFM advisors to work with the AFAD directors to develop recommendations for clarifying the role that AFAD can execute to prepare consolidated financial reports for MOF review and approval. The local financial audit consultant will work with the AFAD directors to draft a working paper that covers the analysis and recommendations for the specific role that AFAD should plan in the annual financial reporting process. The local financial audit consultant can then facilitate a meeting between AFAD, FBSA, MOF to discuss and reach agreement on the AFAD role in line with GOI laws and MOF regulations and then follow up to ensure that AFAD directors are implementing their roles as agreed by the AFAD, FBSA and MOF. If needed and decided, the local financial audit consultant can assist in drafting a directive to be issued by the MOF on the role of the AFAD in the annual financial reporting process.

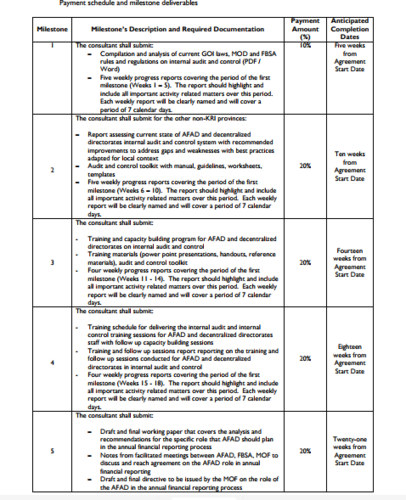

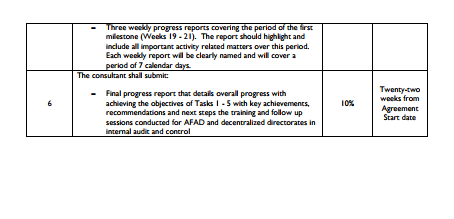

Task 6: Prepare a final progress report in line with IGPA’s guidance. The consultant will prepare a final progress report that details the results of the audit training and capacity building work implemented under this scope of work, recommendations for next steps for the sustainability of the training and capacity building work, and any other recommendations related to the work implemented under this scope of work.

The consultant will also be required to provide weekly reports, success stories in accordance with IGPA guidelines.

III. Required Deliverables:

Task Deliverable

Task1: Review the current GOI laws, MOF and Federal Board of Supreme Audit rules and regulations on internal audit and control related to the AFAD and decentralized directorates.